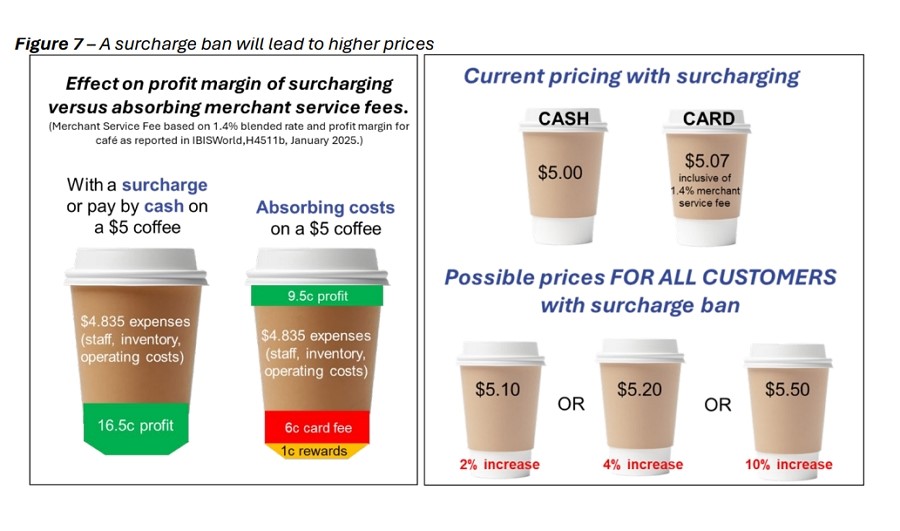

Every time a customer taps their card at your counter, a slice of that sale quietly disappears into the banking system. Currently, many recover some of that expense through a checkout surcharge. Here, I will show you exactly how to use your POS System to protect your margins as the 1 October 2026 surcharge ban deadline hits.

Unlike many people, I was one of the few directly involved in the discussion about the Reserve Bank of Australia (RBA) ban on surcharges, and that is why, after reading some of their advice, which I found almost useless and self-serving, I wrote this article.

Key Takeaways

- The 2026 RBA surcharge ban legally prevents retailers from passing card processing fees directly to customers at the checkout.

- Least-Cost Routing (LCR) directs debit payments to the cheapest network but requires manual activation by the retailer.

- Blended merchant rate plans will hide the proposed fee reductions unless retailers switch to interchange-plus pricing.

- Many fixed-price stock items force shops to absorb payment costs completely because retail prices cannot be raised.

- Premium reward credit cards remain highly expensive to process and will cut deeply into retail profits.

- No-cost EFTPOS providers must alter their entire business model, leaving retailers vulnerable to sudden fee introductions.

- Modern Point of Sale (POS) software allows retailers to find products that can absorb the price bump.

What is the 2026 RBA Surcharge Ban?

The 2026 RBA Surcharge Ban, effective October 1, 2026, prohibits Australian retailers from adding checkout fees to Visa, Mastercard, and EFTPOS transactions. This ensures consumers see a single final price without surprise charges. For example, a retailer can't add a 1.5% fee on a $20 book to cover banking costs. However, this ban only covers processing costs, not penalty rates for weekends or holidays. Retailers can still charge holiday surcharges if they are clearly disclosed, such as a 10% Sunday surcharge at a cafe, excluding card-specific fees.

The RBA surcharge ban starts on 1 October 2026 for all domestic card networks.

The RBA combined a ban on interchange fees with mandated reductions, which are hidden charges your bank pays to card networks for transaction approval. For instance, the fee for verifying funds with Visa is capped at a lower rate.

Why the 2026 RBA Surcharge Ban Matters for Your Bottom Line

The 2026 RBA Surcharge Ban shifts the burden of payment processing directly onto retailers. This matters because the fundamental cost of processing electronic payments does not disappear; the RBA wants it to be an invisible operating expense. For example, a shop processing $500,000 in card sales annually will instantly lose $7,500 in pure profit if it previously charged a 1.5% fee to its customers.

Card payments cost the Australian economy over $1.6 billion annually.

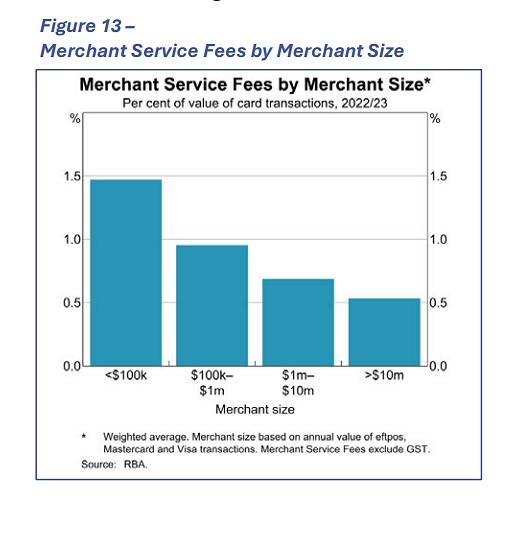

Consequently, SMB shops face a structural disadvantage compared to massive supermarket chains. Large acquirers and major retail chains can negotiate ultra-low processing rates directly with banks due to their massive transaction volumes. For example, while an independent newsagency might pay 1.2% per tap, a supermarket giant next door might pay a fraction of a cent per transaction.

Are Cash Discounts Still a Legal Alternative to Surcharging After October 2026?

YES. Cash discounts remain a fully legal and compliant pricing strategy for retailers who want to encourage customers to use cash. The Reserve Bank explicitly allows businesses to display a standard shelf price and reduce it at the register for cash. For example, you can price a greeting card at $8.00 on the shelf, but program your pos system to automatically drop the price to $7.80 when the cashier selects the cash payment button.

However, relying on cash discounts is a severely limited strategy in today's digital economy. Almost all consumers have shifted overwhelmingly to cards, meaning a cash incentive will capture only a small percentage of your traffic. For example, putting up a sign offering a 2% cash discount will not convince many busy parents to walk to an ATM.

Therefore, cash discounts can make only a minor contribution to your overall margin protection strategy. You must combine this tactic with rigorous merchant-fee negotiations and smart inventory pricing to protect your entire business.

Do Premium Reward Credit Cards Cost Small Retailers More After the Surcharge Ban?

Premium reward and corporate credit cards incur higher interchange fees than standard debit cards mainly because of their point structures, and under the 2026 surcharge ban, Australian retailers must absorb these costs now in full. These luxury cards fund their points programs by charging the merchant more. This practice should be illegal, as the merchant is being forced to pay the bank's marketing. The RBA did not seem to care about that. For example, processing a standard EFTPOS debit card might cost your shop 14 cents, but tapping a platinum frequent-flyer credit card for the same purchase might cost you 80 cents.

Some shops will be hit much more if they sit in an affluent suburb, where customers are actively chasing airline points and cash-back rewards on every small purchase. For example, a customer buying a simple $5.00 newspaper might tap a corporate credit card, with higher fees.

However, because Amex has notoriously high fees and is not local, you will be legally permitted to refuse their cards. For example, you can stick a clear "No Amex" sign on your front door and configure your pos system to decline those specific cards automatically.

Are You Caught in the Blended Rate Trap for Merchant Fees?

This is important: blended merchant fees include the true cost of card processing by charging a flat percentage across all card types. Banks have been aggressively selling these simple flat-rate plans, but they are incredibly dangerous when the wholesale fees drop.

The upcoming RBA wholesale caps will, as such, not automatically save you money if you remain on such a plan. When the government forces banks to lower their interchange fees, the banks may not be legally required to pass those savings on to retailers under flat-rate contracts. If so, the bank will enjoy a wider profit margin on your transactions while you continue paying the same 1.5% fee.

Therefore, you must contact your bank immediately and review your pricing. Ask about the "Interchange-Plus" pricing model. It is transparent and charges you the exact wholesale cost of the card plus a small, fixed bank markup. For example, on an Interchange-Plus plan, when the RBA drops the wholesale cost of a debit transaction, only then will your monthly merchant bill drop.

How Does Least-Cost Routing (LCR) Lower Debit Card Costs?

Least-Cost Routing (LCR) is a payment terminal feature that automatically directs debit tap-and-go transactions through the cheapest available network, typically EFTPOS, reducing per-transaction costs for Australian merchants. Almost all businesses will be better off under this scheme. However, most businesses do not have it, and, unfortunately, the Reserve Bank has not legally required banks to enable this money-saving feature. This means most retailers are currently paying higher fees simply because they have not activated it. If so, you must take proactive steps now to fix this in your business. Pick up the phone, call your EFTPOS provider, and explicitly demand that Least-Cost Routing be activated. If your provider refuses or claims their older terminals cannot support the feature, it is time to shop for a new EFTPOS provider immediately.

What Should You Do If You Use a No-Cost EFTPOS Provider?

If you are using a zero-cost EFTPOS provider, you are not actually getting free banking; your customers are simply paying your merchant fees via an automatic surcharge.

From 1 October 2026, the RBA will make it illegal to pass card fees directly to consumers at the point of sale. Because zero-cost providers rely entirely on consumer surcharges for their revenue, their current business model probably reverts to charging retailers directly. They cannot legally continue providing you with free hardware and 0% merchant rates.

Now, traditional banks can comfortably keep charging you a flat 1.5% merchant fee behind the scenes, and what you will see is that the zero-cost providers will rewrite their contracts.

Recently, I contacted a major no-cost EFTPOS provider on behalf of my clients to ask about their business model after October 2026. They admitted they were still digesting the information and needed time to figure out their post-ban pricing strategy.

Therefore, if you use one of these providers, you must demand answers about your future contract terms. I suggest contacting them in June after they have had some time to work it out.

How Do You Handle Fixed-Price Inventory vs Flexible Inventory?

Fixed-price inventory is products you do not control, such as lottery tickets, goods with retail prices printed on them, etc. The retailer cannot adjust the shelf price. These items are considered the biggest problem now.

Consequently, you cannot treat your shop as a single, average-profit pool. You need to identify which departments can carry slightly higher prices without being aggressive.

What Dates Should Retailers Put in the Diary?

We have a strict timeline due to regulatory deadlines, Unfortuanely they don't match retail realities. The government has created a transparency gap. The ban begins in October 2026, but major banks won't publish actual pass-through rates until late January 2027. This leaves you blind during Christmas.

Info: Large acquirers must publish wholesale fee data by 30 October 2026.

Foreign card interchange caps take effect on 1 April 2027, but we are still awaiting details.

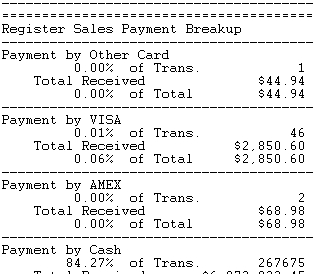

How Can Your POS System Automate Margin Protection?

Your POS system can act as your primary defence against shrinking retail margins. Rather than guessing which items can absorb price bumps, your software provides hard, irrefutable data on category profitability. For example, you can run a GMROI (Gross Margin Return on Investment) report to discover exactly which gift lines sell quickly at a high margin, marking them as prime candidates for a small price increase.

Furthermore, modern POS software allows you to execute these defensive strategies in bulk, saving you days of manual data entry. Once you decide to increase your novelty stationery category by 3%, the software does the heavy lifting. For example, you can use the bulk price update tool to instantly raise prices on 400 separate stationery items with a single click, instantly updating the barcode database.

Your POS system tracks changes in real-time, showing if adjustments like a 40-cent price increase for premium greeting cards impact sales. If sales stay steady, you've recovered fees without losing customers.

What Steps Should You Take Before October 2026?

Retrieve your latest merchant statement and scrutinise it immediately. This document holds your current financial exposure to card fees. For example, identifying exactly how much you pay in scheme fees, terminal rentals, and percentage rates gives you a baseline to measure any future bank promises against.

Next, execute this strict operational checklist to secure your business:

- Contact your bank to confirm your current pricing model.

- Demand written activation of Least-Cost Routing for all terminals.

- In June, if you use a no-cost EFTPOS provider, find out their exact post-October fee structure.

- Run category margin reports to separate fixed-price from flexible inventory.

- Strategically raise prices on flexible, high-margin categories before August.

Finally, communicate with your staff so they understand why signage and checkout processes will change. For example, training your team on how to explain the disappearance of surcharges smoothly prevents awkward conversations at the register when the October deadline arrives.

Conclusion

The 2026 RBA surcharge ban is a profound structural shift that forces Australian retailers to manage hidden costs intelligently. While the government narrative focuses on consumer fairness, the reality is more than that.

Written by:

Bernard Zimmermann is the founding director of POS Solutions, a leading point-of-sale system company with 45 years of industry experience, now retired and seeking new opportunities. He consults with various organisations, from small businesses to large retailers and government institutions. Bernard is passionate about helping companies optimise their operations through innovative POS technology and enabling seamless customer experiences through effective software solutions.