The RBA has officially decided to ban card surcharges in its RBA conclusion paper here. This means that come October 2026, you will no longer be allowed to charge a surcharge for Debit and Credit Card purchases. However, you will still be able to offer a cash discount.

Key Takeaways

- The surcharge ban is a new federal rule starting in October 2026 that prevents retailers from charging extra checkout fees.

- Many will, as a result, see their Profit margins shrink on fixed-price goods, e.g., magazines, lotto, etc

- Interchange fee caps will drop, helping lower the wholesale cost you pay banks for card processing.

- Cash discounts are still completely legal and offer a smart way to avoid card fees.

- POS software gives you the power to update prices in bulk and track your exact margins in real-time.

- Premium cards, the RBA claims that the fee gap between debit and credit cards will be reduced.

- The RBA has asked for clearer transparency rules on hidden bank fees.

- You can still reject American Express

What is the 2026 RBA Surcharge Ban?

The 2026 RBA Surcharge Ban is a federal rule that takes effect in October 2026 and prevents Australian retailers from adding surcharges to card payments at checkout. This new rule forces business owners to pay the full cost of card processing out of pocket. For example, if a customer buys a $10 notebook with a rewards credit card, you cannot add a 1.5% fee to cover the extra credit fees charged by the bank.

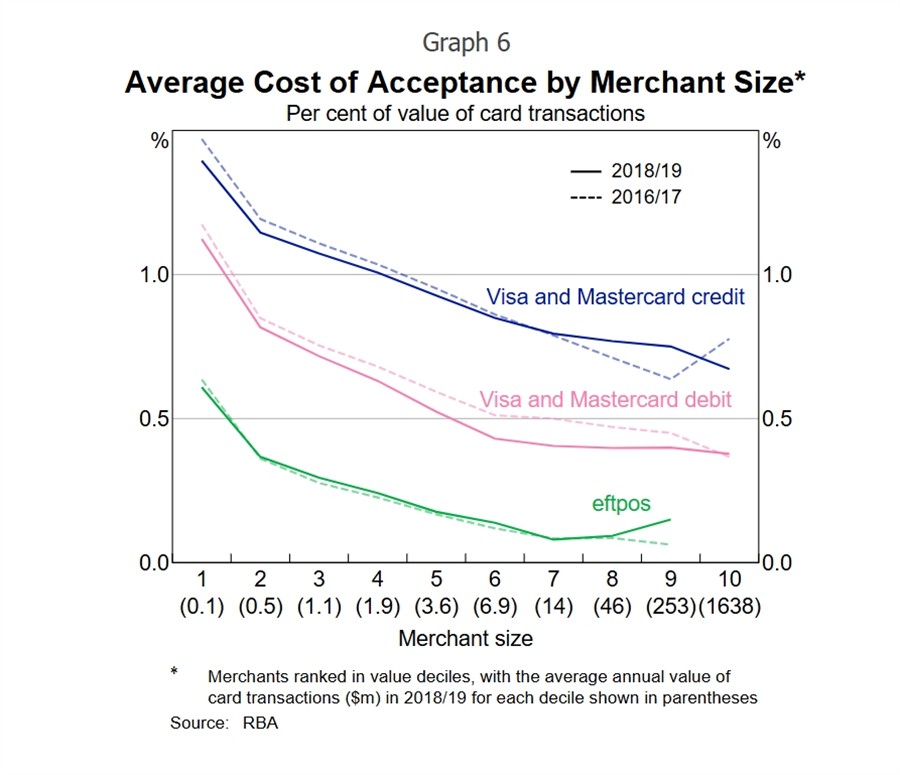

Next, the RBA mandated a reduction in one of the bank fees (interchange fees) to help businesses cope. Interchange fees and scheme fees are the hidden wholesale costs that your bank and the card networks charge you to process every electronic transaction. When a customer taps their card, the payment network takes a tiny slice of the sale before the money hits your account. For instance, Visa and MasterCard charge a fee just to use their global networks to verify that the customer has enough money. This should reduce some of the fees merchants are charged.

Also, by forcing banks to publish these fees, the RBA hopes to increase competition. If you know exactly what your bank charges compared to other banks, you can negotiate a much better deal for your store.

Did the RBA Fix the Gap Between Small and Large Merchants?

The RBA claims to close the gap between small and large merchants by strictly limiting the maximum interchange fees banks can charge. You will need to actively check your merchant statements to ensure your bank actually passes these savings down to your account. Do not assume your bank will automatically lower your bill.

The problem of Premium Credit Cards

These cards affect your margins by imposing significantly higher processing costs. Soon, you will no longer be able to recover via a checkout surcharge. RBA thinks that lowering interchange fees will help here, which it will, but only to a limited extent. I am sure merchants will end up having to keep paying for the lavish rewards programs attached to platinum travel cards. For instance, processing a basic debit card might cost you 10 cents, but processing a premium platinum card now costs you over a dollar for the same sale. If a customer tries to pay with a premium Visa or MasterCard, and your terminal can accept them, you must also accept their premium cards, even though they carry higher fees. Mind you, in reality, often you do not know until the transaction has gone through whether it is one of these cards.

American Express

You have complete control over whether you accept American Express. If you feel their rates are too high to match the new 2026 realities, you are entirely within your rights to put up a 'No Amex' sign and turn it off on your POS system.

Will the Surcharge Ban Cause Retail Price Inflation?

The surcharge ban will cause retail price inflation because shops must raise the cost of their goods to absorb the banking fees, which everyone agrees on. The RBA optimistically estimated that this policy would have only a tiny, 0.1%, one-off inflationary effect across the whole economy. We will see whether they are right.

How to Manage Fixed-Price Inventory

These are items where the merchant cannot change the fees. Products such as lottery tickets, newspapers, and phone credit do not offer flexibility for recovering absorbed bank fees. For example, if a magazine publisher prints a strict $9.95 price on the cover, you must swallow the card processing fee entirely. This needs to be addressed ASAP, as the solution proposed of keeping a fixed price item like a magazine at $9.95 but raising the price of a greeting card from $5.00 to $5.50 to balance your overall shop profit, is not workable in the current economic environment.

Why Are Cash Discounts the Best Alternative to Surcharging?

This is the only solution; cash discounts are completely legal price reductions offered to customers who choose to pay with physical notes and coins instead of cards. While the RBA banned card penalties, it openly supports offering price breaks to cash-paying customers. For example, you can price a hardcover book at $20 on the shelf, but program your till to give a 1% discount for cash. Our POS System can be set to do this automatically. Many customers will appreciate the savings. If you are going to do this, put a big sign up so everyone knows.

Automating Real-Time Margin Calculations

When new items, like gifts, come into the shop, you now need to factor in a percentage for bank fees into your pricing. Again, your POS System should be able to handle this automatically.

What Steps Should Retailers Take now?

Retailers must actively audit their current banking costs and overhaul their store pricing strategies long before the October deadline. Do not wait until the last minute. Follow these three steps to protect your store:

Call your bank: Contact your merchant facility provider today and demand a clear breakdown of your current fees. For instance, ask your bank exactly what percentage you pay for standard debit versus premium rewards credit cards. You need to know your baseline costs.

Audit your inventory: Review your stock to identify which high-margin items can safely handle a small price increase. For example, find your best-selling toys or gifts and plan a small price bump.

Fixed price items: You need to review these now. Ask your suppliers what they plan to do about your margins on these items.

FAQ

Q: What's the current status on the RBA banning card surcharges? Is it actually happening?

A: Yes, this is Labor policy and is almost certainly going to come into effect.

Q: Will cafes and shops just jack up the price of everything to cover the ban?

A: Yes, you will likely see the cost of card processing baked into the everyday sticker price of items, similar to GST. Some shops may adopt a discount-for-cash policy.

Q: Why don't they just cap the merchant fees as they do in Europe?

A: Good question, I think that is what they should have done. What many lobbied heavily for in Australia was a more targeted fix, of banning surcharges only on debit cards or low-value transactions, as New Zealand did. This was unfortunately rejected.

Q: Are weekend and public holiday surcharges getting banned too?

A: No, the RBA's proposed ban only targets payment processing surcharges, the 1% to 2% fee applied when tapping your card. Weekend and public holiday surcharges are legally separate and designed specifically to cover mandated penalty rates for hospitality and retail staff.

Q: Does the ban apply to both credit and debit cards, or just EFTPOS?

A: The changes aim to eliminate surcharges across all major networks, meaning it would apply to Eftpos, Visa, and Mastercard debit and credit transactions. The ultimate goal is to mandate that the price you see on the shelf or menu is the exact total you pay at the till, regardless of your card type.

Q: How are small businesses supposed to absorb these costs without going under?

A: You can ask your customers to support your local shops by selecting the Savings account, which routes the payment through the cheaper Eftpos network rather than Visa or Mastercard.

Q: Who actually benefits from this? Won't the banks, Visa and Mastercard just keep making billions?

A: Well, the big banks, Visa and MasterCard are certainly winners, but to be fair, consumers will benefit from transparent, upfront pricing.

Q: Why am I being charged a percentage fee for tapping when the technology costs the same?

A: A good question, as it costs as much to process a $1 transaction as a $100 transaction.

Q: Is this just a push to make us a cashless society?

A: I think so.

Q: If a shop is still charging me a tap fee right now, are they breaking the rules?

A: No, it is still entirely legal for merchants to charge a card surcharge, provided it is not excessive and only covers their exact cost of acceptance. The ban only starts in October. This gives retailers a transition period to adjust their pricing models and negotiate new merchant terminal rates with their banks.

Q: How are we supposed to absorb the high costs of premium credit cards without going under?

A: People are expecting a price rise as the actual cost of processing payments has not disappeared; most businesses will have to put these bank fees into their standard shelf prices.

Q: Why do big retailers like Coles and Woolworths get away without surcharging, but we get slammed?

A: Large retailers indeed process an enormous volume of transactions, so giving them the leverage to negotiate significantly lower merchant fees with the banks and card networks than smaller retailers who lack this bargaining power, but what I have noticed is that most of these retailers have quietly given up surcharging a while ago.

Q: Is the government doing anything to lower the actual merchant fees we pay to the banks?

A: Yes. Alongside the surcharge ban, the RBA is requiring banks to disclose previously hidden fees and is enforcing strict reductions on interchange fees. The RBA estimates that 90% of smaller businesses will be better off under the lowered wholesale caps, though most of us remain deeply sceptical.

Q: What happens if we just keep our surcharges active after October 2026?

A: Once the ban comes into full effect, applying a card surcharge will be a breach of consumer law. Non-compliant retailers will likely find that this is a matter for the courts.I would not suggest doing this.

Written by:

Bernard Zimmermann is the founding director of POS Solutions, a leading point-of-sale system company with 45 years of industry experience, now retired and seeking new opportunities. He consults with various organisations, from small businesses to large retailers and government institutions. Bernard is passionate about helping companies optimise their operations through innovative POS technology and enabling seamless customer experiences through effective software solutions.