Australia's Cash-In-Transit Crisis part 2

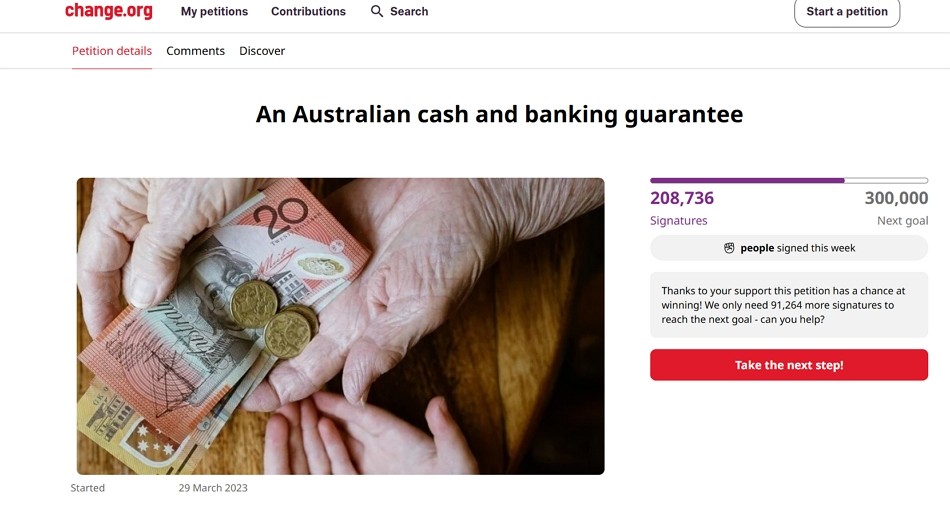

Readers here already know that the temporary Armaguard bailout that has been keeping Australia's cash-in-transit network afloat expires on 30 June 2026. Less clear is exactly how the incoming new pricing model will affect us after that.

Key Takeaways

- A cash-in-transit crisis is a severe disruption to Australia's physical cash collection network that threatens to raise retail costs.

- Utility-style pricing will charge businesses based on distance, severely impacting independent retailers across regions.

- Point-of-sale (POS) systems provide the exact tender-mix data needed to forecast your margin exposure.

- Financial auditing of your recent bank statements reveals your current baseline cash expenses before new fees apply.

What Is the Cash Crisis?

Australia's cash-in-transit crisis, spoken about here, is the financial instability threatening the cash infrastructure that collects, transports, and processes cash. Currently, the dominant provider, Armaguard, relies on a temporary bailout to keep its armoured trucks running. Armaguard funding arrangements officially end on 30 June 2026. We now know that new funding models will shift the financial burden directly onto end users, which is confirmed and will soon start. The inevitable cost increases for retailers begin soon.

Why the Cash Crisis Matters

The cash-in-transit crisis matters because it will fundamentally alter the cost of doing business for retailers that accept cash. Major supermarket chains will leverage their massive daily volumes to negotiate better cash contracts, leaving smaller players exposed. Up to now, regardless of size, independent retailers have been able to compete equally with the majors on cash handling.

Furthermore, regional businesses face an extreme risk under the new model. If distance-based pricing takes effect, this will accelerate the current increases in banking charges for manual cash deposits that the industry is quietly seeing.

Tracking Cash With POS Systems

The first point is to get real figures for what you are banking. Review the bank deposit reports in your POS system to see exactly how exposed your business is to cash transactions today. For example, knowing that cash makes up exactly 12% of your weekly revenue gives you the hard data needed to forecast your vulnerability to rising bank fees. Once you have the exact cash figures from your POS reporting, you should approach the bank. Sometimes, the banks can help you restructure your deposit schedules or even waive certain fees. You will not get them unless you approach them proactively.

Conclusion on Cash

We may need to rethink our payment types for our business soon.

Written by:

Bernard Zimmermann is the founding director of POS Solutions, a leading point-of-sale system company with 45 years of industry experience, now retired and seeking new opportunities. He consults with various organisations, from small businesses to large retailers and government institutions. Bernard is passionate about helping companies optimise their operations through innovative POS technology and enabling seamless customer experiences through effective software solutions.