Stop Retail Cash Leaks

Running a retail shop or newsagency involves managing foot traffic, staff, and stock, but often overlooks cash flow. The gap between paying suppliers and waiting for sales to convert to cash drains working capital.

Key Takeaways

- Retail cash flow is the critical timing gap between money exiting the business for inventory and returning through customer sales.

- Inventory management requires identifying slow-moving stock that traps working capital and prevents investment in high-value items.

- Credit control policies dictate setting strict limits for customer accounts, regardless of the client's size or government status.

- POS systems automate credit decisions by enforcing warning thresholds and blocking transactions when accounts exceed their limit.

- Cash flow forecasting involves tracking weekly cash inflows and outflows to predict shortfalls before supplier invoices become overdue.

What is Retail Cash Flow?

Fundamentally, retail cash flow is the net balance of cash moving into and out of a retail business at any given time. It represents the actual cash you have on hand to pay the bills, rather than the theoretical profit. It is all too easy for a retailer to show strong profits on paper but have those profits tied up in massive stock orders, leaving the owner still struggling to pay staff wages.

Consequently, understanding this difference is the first step toward budgeting stability. Profit indicates that you are making money, whereas cash flow dictates whether you have the actual funds available when you need them.

Therefore, comprehending this timeline entails careful review of your cash flow management. When you bridge the gap between paying out and getting paid, you instantly reduce the stress of running an independent shop.

Unfortunately, poor cash management is a silent killer in the Australian retail industry, and the problem is not getting better.

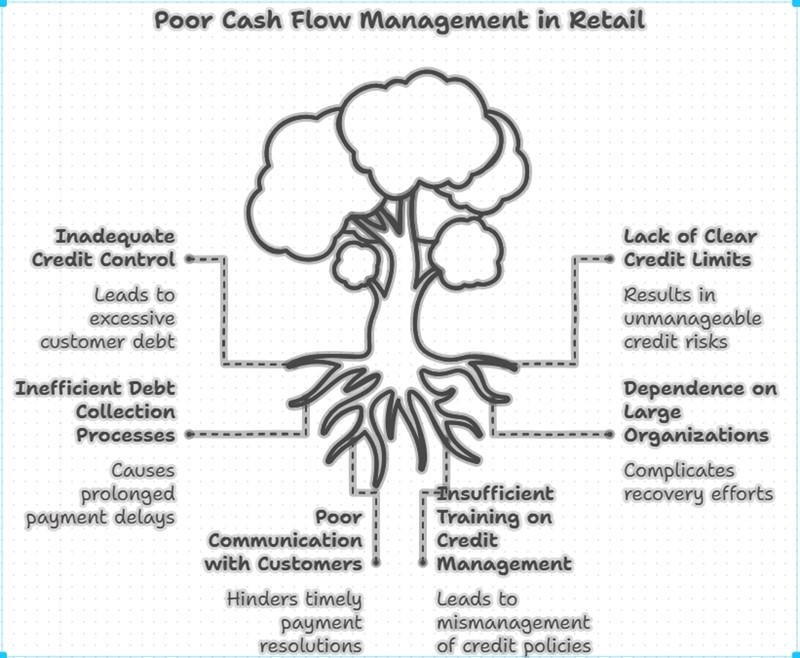

What Are the Most Common Cash Flow Problems in Retail?

Usually, the most common cash flow issues in retail are slow-moving stock, overdue customer accounts, and poorly timed supplier payments. These problems don't usually make a loud noise; instead, they gradually choke your working capital over several months.

The Trap of Dead Inventory

Primarily, slow-moving inventory penalises your business twice: it depletes your cash reserves during purchase and paralyses your buying power while sitting unsold. Every item sitting unused on a shelf is, in effect, a stack of five-dollar bills you cannot use to pay your electricity bill. For example, holding onto last year's calendar stock in February is a direct drain on your shop's working capital.

Thankfully, modern reporting tools in your POS System can identify these items. Use your old and dead stock reports at least monthly.

Over-Ordering Without Data

Similarly, buying stock on a gut feeling rather than hard data is a guaranteed way to freeze your cash. Buyers often order heavily into new product lines, hoping for a trend, only to find their customers are not buying them. For example, a client of ours a boutique gift shop ordered a pile of expensive imported candles that looked great at a trade show, only to find their budget-conscious local shoppers completely ignore them.

Another problem occurred when a salesman from a greeting card company helped one of our clients place a large order, but no one checked the existing stock in the storeroom in the back. Piles of cards just sat uselessly there, eating the cash flow.

Use Automatic orders do not kid yourself the computer will win

How Do Overdue Customer Accounts Restrict Retail Cash Flow?

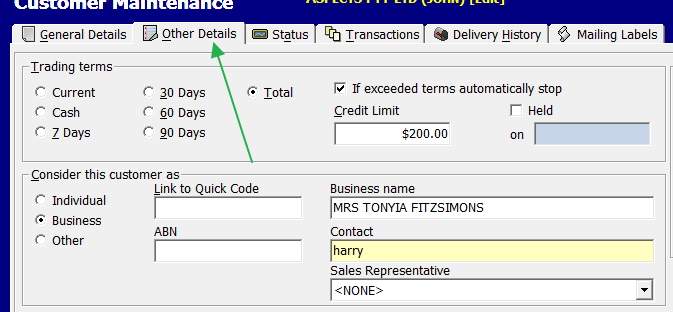

Undeniably, overdue customer accounts restrict retail cash flow by forcing your business to act as an unpaid bank for its clients. Extending credit to local schools, sporting clubs, or corporate offices feels like a great way to secure loyal business, but it comes with immense financial risk. Many of these will eat up your cash flow, leaving you waiting 90 days for their corporate office to settle their monthly invoice. Use credit limits which are easy to setup.

The Myth of the "Safe" Corporate Client

Interestingly, large organisations and government departments are often the worst offenders when it comes to timely payments. While you might assume a massive account is perfectly safe, its size actually makes it harder to collect from due to complex internal bureaucracies. For example, a government agency might have the funds, but their strict accounts payable policies mean your invoice will not be processed for a minimum of 60 days. Threatening legal action rarely works, the employees often do not care and/or there is nothing they can do, they work to organisational policy.

Years ago, I was stunned when I had a cheque from a goverment agency bounce as the bank said they had insufficient funds.

Consequently, you must lay down clear credit limits from day one, rather than allowing a customer to quietly accumulate unmanageable debt. Its easy to set up.

Introducing Proactive Credit Warning Thresholds

Furthermore, proactive credit management requires catching the problem ASAP. Relying on staff to manually remember who owes what during a busy lunch rush is a recipe for disaster. For example, one of my clients happily hand over $200 worth of stationery to a local school teacher, completely unaware that the school's account was already 45 days overdue.

How Does a POS System Automate Credit and Inventory Tools?

Essentially, a modern Point of Sale (POS) system automates your credit and inventory tools by hard-coding your financial policies promptly into the checkout process. It removes the emotional difficulty of cutting off a loyal customer by letting the computer be the "bad guy." For example, when a customer attempts to charge items to an account that is over its limit, the system simply blocks the transaction and forces the operator to request immediate payment. That is actually the best place to collect a debt, when the customer is standing directly in front of you, wanting more goods.

Assessing Traditional vs. POS-Automated Cash Flow Management

Naturally, making the leap from manual observation to automated POS controls represents a massive operational shift. Here is how automating the areas immediately impacts your cash flow:

- Credit Limits: Relying on staff to guess or check a paper ledger leads to sudden debt accumulation. Conversely, a pos system automatically enforces hard limits, preventing uncontrolled financial exposure.

- Warning Alerts: Traditionally, owners only notice bad debt during an end-of-month review. An automated system manages this by alerting the cashier at the 70% threshold, permitting early intervention before the maximum limit is reached.

- Inventory Reorders: Manual buyers rely on hunches and empty shelves, which frequently ties up cash in dead stock. A modern system uses historical data to suggest precise, data-backed orders.

- Account Increases: Casual approvals at the counter create immense risk. The system requires a formal review process in the back office to ensure credit is only given to proven payers.

- Pricing Strategy: Applying manual markups is often inconsistent. Utilising AI retail pricing algorithms can optimise your margins and automatically maximise the profit per item sold.

Following Steps for Retail Cash Flow Management

You need to transition immediately away from reactive debt collection and emotional inventory purchases. Actionable cash flow management starts with creating boundaries today so you do not have to chase bad money tomorrow. For example, informing all account holders this week that standard terms are moving to 14 days will immediately pull your cash cycle forward.

First, start new accounts with very small limits to test their payment reliability. Let the amount build up only after they have proven they can pay on time, and be certain to review all existing credit limits annually. For example, start a new corporate client on a $200 limit, and only raise it to $500 after three consecutive months of on-time payments.

Additionally, consider whether a customer actually needs an in-house credit account. With the widespread availability of business credit cards and Buy Now Pay Later (BNPL) services, you can often shift the credit risk entirely to a third-party financier. For example, running a high-value transaction through a BNPL provider guarantees you get paid immediately while the customer still gets to pay in instalments.

Stop Guessing and Start Controlling Your Retail Cash Flow

If your existing system cannot automatically block overdue accounts, warn staff at checkout, or identify dead stock that is draining your capital, it is time for an operational upgrade.

Written by:

Bernard Zimmermann is the founding director of POS Solutions, a leading point-of-sale system company with 45 years of industry experience, now retired and seeking new opportunities. He consults with various organisations, from small businesses to large retailers and government institutions. Bernard is passionate about helping companies optimise their operations through innovative POS technology and enabling seamless customer experiences through effective software solutions.