Integrating video surveillance and the POS system

Integrating your video surveillance with the POS system makes a lot of sense. This example shows a skimmer being installed by some shop thieves. Your staff may not be involved in the fraud at the point of sale. This fraud took three (3) seconds. Nothing would show here on the computer if the cameras had never been installed on the tills; it would never have been found.

It took three seconds. On the footage, a thief leans over the till, slips a skimmer onto the terminal, and walks out of the shop. No alarm. No confrontation. If a camera hadn't been pointed at that till, nobody would ever have known it happened.

That clip says everything about why the point of sale is the most important place in your shop to put security cameras. The tills are where the cash is, and that's where most of the fraud happens. Which is exactly why integrating your video surveillance with the POS system makes so much sense.

Most fraud looks like a normal sale.

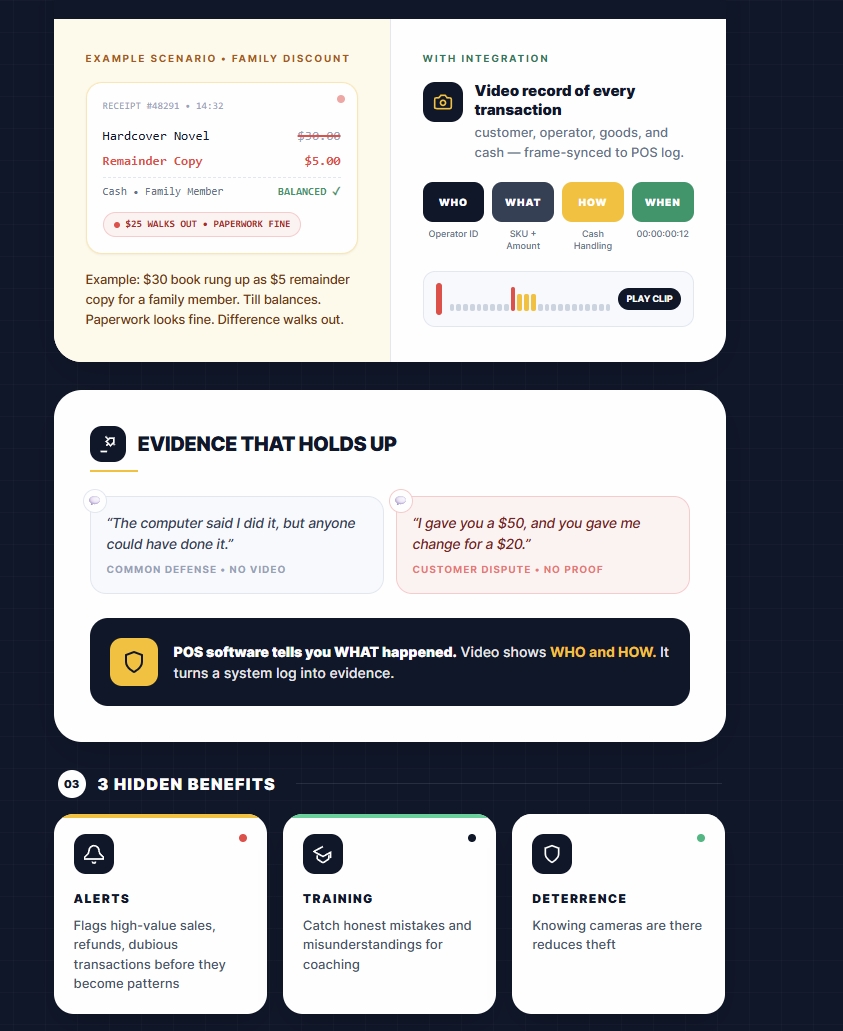

The skimmer case is an extreme example. Most POS fraud involves real transactions that are quietly manipulated. The classic pattern: a staff member's brother picks up a $30 book, and it gets rung up as a $5 remainder copy. The till balances, the paperwork looks fine, and the difference walks out the door.

With an integrated system, you have a video record of every transaction — the customer, the operator, the goods, and the cash. When the numbers don't add up, you're not left guessing.

Evidence that holds up

POS software alone tells you what happened in the system — not who did it, or how. That becomes a real problem the moment a dispute needs to be verified. Anyone who has dealt with these cases will recognise the lines you hear in court:

"The computer said I did it, but anyone could have done it."

"I gave you a $50, and you gave me change for a $20. Okay, the computer says $20, but I gave you a $50."

Video settles those arguments. It turns a system log into evidence.

Alerts, training, and deterrence

An integrated system doesn't just record — it flags. High-value sales, refunds, and other dubious transactions can trigger alerts, pointing you toward possible fraud before it becomes a pattern. And not everything you uncover will be fraud. Often, it's just common mistakes or misunderstandings that can be corrected with a little additional training.

Then there's the simplest benefit of all: just knowing the cameras are there has been shown to reduce theft in the first place.

Cameras alone aren't enough.

You may already have cameras over the tills. But if the video isn't integrated with the POS, every investigation means scrubbing through archived footage by date and time to find the transaction you need. It's slow, and it's a pain. Integration ties each transaction to its clip, so you go straight to the moment that matters.

Beyond the basics

Once your cameras are integrated, they can do more than record transactions. The same setup can support:

- Facial recognition analytics to identify known individuals the moment they walk in.

- People-counting analytics to make sure occupancy limits are never exceeded.

- Demographic analysis to better understand who is shopping, and when.

The tills are where the cash is. Make sure they're also where the evidence is.

Written by:

Bernard Zimmermann is the founding director of POS Solutions, a leading point-of-sale system company with 45 years of industry experience, now retired and seeking new opportunities. He consults with various organisations, from small businesses to large retailers and government institutions. Bernard is passionate about helping companies optimise their operations through innovative POS technology and enabling seamless customer experiences through effective software solutions.